We take the responsibility of managing our clients’ wealth very seriously. We also believe in Setting A Great Example (SAGE) through building our communities, working with charities and educating investors of all ages.

The team shares a strong commitment to professionalism and development. We are constantly striving to keep ahead of the rapid changes in this increasingly complex world, and to improve our performance in the three key areas we serve our clients: investment returns, wealth management advice, and client care.

Are you Retirement Ready?

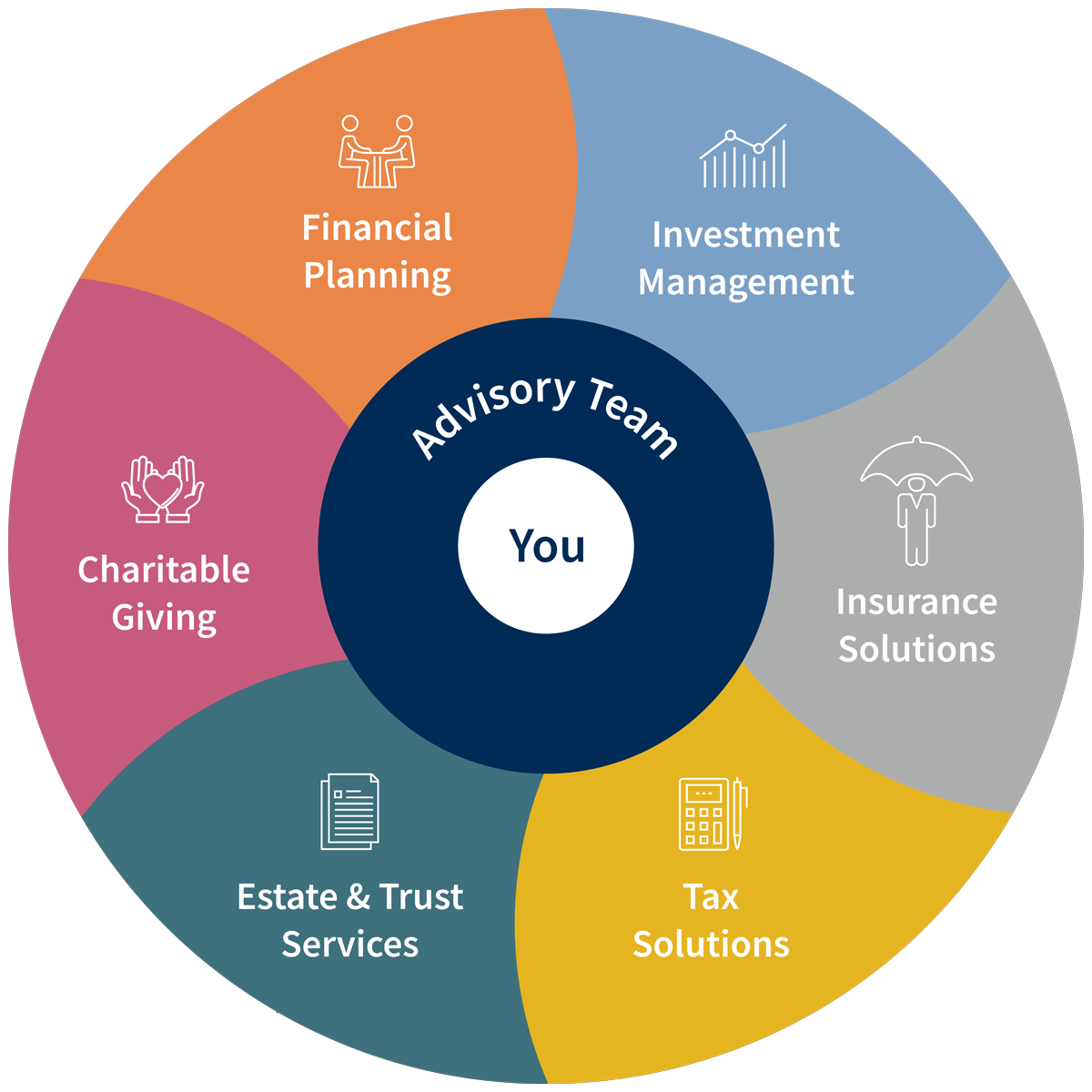

Your success in retirement depends on the planning you do today. No matter what stage you are at now, we have the Total Wealth Solutions to help you achieve your financial goals and build your legacy.

Who We Work With

The gratification of wealth is not found in mere possession or in lavish expenditure, but in its wise application.

Miguel de Cervantes

Information & insight

![]()