5 things for advisors to know ahead of U.S. elections

Clients will have questions. Here’s a guide that explains how to answer them

By Anu Gaggar, CFA®, FRM

Key takeaways

- History shows that markets have been generally nonpartisan as it relates to presidential elections and that elections have not definitively determined market returns.

- Specific economic policy proposals are difficult to turn into smart tactical investment decisions.

- The upcoming election provides an opportunity for advisors to guide clients toward better decisions that are free from emotion and to review life events and goals, allocation mix, and any changes in risk tolerance.

It’s instinctive to wonder how U.S. election cycles might impact the economy, market sentiment, investment performance, and the outlook for specific sectors and asset classes.

For advisors, however, it’s critical to remain focused on the fundamental tenets of asset allocation.

Following are my five takeaways regarding the 2024 U.S. election. They provide a framework so advisors can accurately answer clients’ questions regarding how much (or how little) the 2024 election cycle could impact the investment landscape. In doing so, advisors can use the opportunity to engage clients and keep them on track to achieve their long-term investment goals.

1. U.S equity markets have been largely nonpartisan

Since 1933, stocks have performed better under Democratic presidents (Exhibit 1). That said, the party that’s been better for the stock market over the long term has differed based on the timeframe studied and whether annualized results were calculated using a mean or a median, for instance. There hasn't been a clear edge based on the party in control of the White House. Other political factors—such as whether Congress is divided—have had more influence on market performance over many years.

Exhibit 1: Annualized average S&P 500 performance, March 1933 to September 2024

Past performance is no guarantee of future results. Data analyzed daily going back to March 4,1933. Source: Fidelity Investments and FactSet Research as of 10/1/24.

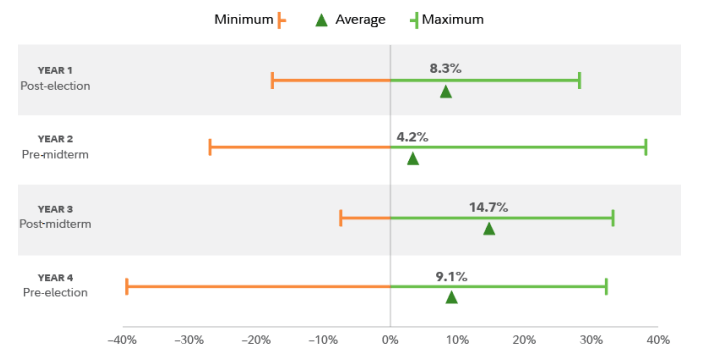

Elections themselves have not impacted average market returns nearly as much as some might think. Going back to 1950, the range of market outcomes has tended to be the widest in the 12 months before a presidential election and the narrowest in the year following midterm elections (Exhibit 2). However, the average returns in each of the four years do not point to a clear trend driven by the political cycle. Bottom line: Stock returns have been driven far more by the strength of the U.S. business cycle, consumer spending, and corporate profit growth than the party in the administrative office.

Exhibit 2: Stock market returns between elections, 1950–2023

Past performance is no guarantee of future results. Data spans from November 30, 1950, to November 14, 2023. Years represent the 12- month period from November 30 to November 30 following a U.S. presidential or midterm election. The chart depicts the average, minimum, and maximum price return achieved during this period. Stocks are represented by the S&P 500®. Indexes are unmanaged. It is not possible to invest in an index. Source: Haver, FactSet, FMR. As of November 14, 2023.

2. Specific economic proposals may matter only on the periphery

Some specific economic proposals by presidential candidates could influence aspects of the market in the coming years. However, it’s unclear which proposals have been put forward solely to score political points and which ones could make their way to the floor of Congress and be enacted. Thus, it is difficult to make thoughtful tactical investment decisions based on candidates’ statements on the campaign trail. Try to stay focused on the policy proposals that are an official part of each candidate’s economic policy platform, have enough detail for economists to score and measure the likely economic impact, and are proposals that have a realistic chance of implementation if the candidate wins.

3. Government debt shouldn't be ignored

Both parties have contributed to a ballooning fiscal problem that could be a long-term burden for future generations. As noted by Fidelity’s Asset Allocation Research team, U.S. federal debt has been rising for decades. This was the case even before the COVID pandemic. Servicing the federal debt is now at par with defense spending and is the largest part of the U.S. budget after Social Security—and is an important investment issue for the future. One of the first orders of business for the next president will be renegotiating the U.S. debt limit in January 2025, which may set the course for the year.

The U.S. is not alone. A global debt issue could continue to worsen in the coming decade. Rising global debt could lead to greater experimentation with both fiscal and monetary policy and be a catalyst for a more inflationary economic environment. This could potentially tax the long-term performance of equities and other asset classes, warranting specific changes to strategic asset allocation decisions.

4. Don't dismiss clients' election concerns

Some clients may be genuinely worried about what might happen to their wealth due to the election outcome. This provides an opportunity for advisors to guide clients toward better decisions that are free from emotion and to build stronger relationships by walking clients through the reasons why the election might not be as important to their future wealth as other factors. Depending on the client, the election cycle may be a time to review life events and goals, the allocation mix, any changes in risk tolerance, and proactive tax-management strategies— all factors that are likely to matter over time, regardless of the election outcome.

5. Tax concerns may be real for wealthy clients

No matter who wins, the new president will need to decide whether to extend the individual rate cuts from the Tax Cuts and Jobs Act of 2017 or let many of the provisions sunset in 2025. So far, Trump has said he would extend the 2017 tax cuts. Harris has proposed extending the personal income tax cuts for those making up to $400,000 a year (single) or $450,000 (jointly). For select wealthy clients, it may be appropriate to discuss election potentialities related to income taxes, estate taxes, tax credits, capital gains, social security benefits, and retirement savings. Depending on the client, the election may be an opportunity to proactively discuss Roth IRA conversions that could reduce future tax bills, tax-loss harvesting strategies, and gifts that may lower the value of clients’ estate taxes.

Conclusion

History suggests that the election cycle in and of itself should not be a major concern for most investors. U.S. equity markets have tended to be nonpartisan, and political outcomes have had little, if any, bearing on portfolio outcomes. Election years could see heightened volatility due to headline risks, however. Advisors should remain focused on the fundamental tenets of asset allocation and use the opportunity to engage with clients and keep them on track to achieve their long-term investment goals. Prudent advice to clients is to vote in the booths and not in their portfolios.

Author

Ann Gaggar, CFA®, FRM

Anu is a vice president with the capital markets strategy group at Fidelity Institutional®, which offers financial professionals and institutions access to the investment, technology, and platform solutions they need to service their clients and grow their businesses. She is responsible for formulating and sharing Fidelity’s capital markets views with Fidelity Institutional® clients in the intermediary channel.

![]()

Information provided in, and presentation of, this document are for informational and educational purposes only and are not a recommendation to take any particular action, or any action at all, nor an offer or solicitation to buy or sell any securities or services presented. It is not investment advice. Fidelity does not provide legal or tax advice.

Before making any investment decisions, you should consult with your own professional advisers and take into account all of the particular facts and circumstances of your individual situation. Fidelity and its representatives may have a conflict of interest in the products or services mentioned in these materials because they have a financial interest in them, and receive compensation, directly or indirectly, in connection with the management, distribution, and/or servicing of these products or services, including Fidelity funds, certain third-party funds and products, and certain investment services.

This content contains statements that are "forward-looking statements," which are based upon certain assumptions of future events. Actual events are difficult to predict and may differ from those assumed. There can be no assurance that forward-looking statements will materialize, or that actual results will not be materially different from those presented.

The opinions expressed are those of the speakers or authors and do not necessarily reflect those of Fidelity Investments.

Information presented herein is for discussion and illustrative purposes only and is not a recommendation or an offer or a solicitation to buy or sell any securities. Views expressed are as of the date indicated, based on the information available at that time, and may change based on market and other conditions. Unless otherwise noted, the opinions provided are those of the authors and not necessarily those of Fidelity Investments or its affiliates. Fidelity does not assume any duty to update any of the information.

The Chartered Financial Analyst® (CFA®) designation is offered by CFA Institute. To obtain the CFA charter, candidates must pass three exams demonstrating their competence, integrity, and extensive knowledge in accounting, ethical and professional standards, economics, portfolio management, and security analysis, and must also have at least 4,000 hours of qualifying work experience completed in a minimum of 36 months, among other requirements. CFA® is a trademark owned by CFA Institute.

S&P 500® index is a market capitalization-weighted index of 500 common stocks chosen for market size, liquidity, and industry group representation to represent U.S. equity performance.

Past performance is no guarantee of future results.

Investing involves risk, including risk of loss.

Third-party marks are the property of their respective owners; all other marks are the property of FMR LLC.

Fidelity Investments provides investment products through Fidelity Distributors Company LLC and clearing, custody, or other brokerage services through National Financial Services LLC or Fidelity Brokerage Services LLC (Members NYSE, SIPC).

© 2024 FMR LLC. All rights reserved.

![]()